Excellent news for Kent and Medway based businesses…

Kent and Medway business fund is now accepting applications for 0% loans between £25K – £99K from small and medium sized business start-ups to help develop new and expand existing products, services or processes which in turn can create jobs, drive growth and improve productivity.

Could be this expenditure will quality for generous R&D tax credits too!!!.

Key eligibility requirements

Your business must be able to prove a good profitable track record

Be creating or protecting sustainable jobs

Must not be subject to collections or insolvency proceedings.

Any funding must be 20-30% match funded via business reserves or bank loans.

Please note depending on assessed risk at the discretion of the council further personal security may be required.

Established businesses or those seeking a larger loan can apply for a KMBF Standard loan.

Finer details about both loans and how to apply can be found at

A word of caution when selling your business which contains personal guarantees for the business loans or overdrafts.

A case was reported in the financial press recently where a business owner had sold their business and duly informed their bank of the sale and their desire to be removed from the bank account as they were no longer a director providing the new owner details at the same time. Role forward 18 months and the bank are demanding the old owner repay an overdraft of almost £40K racked up by the new owner who has also filed for insolvency….

The mistake the former owner appears to have made was not asking the bank to remove their personal guarantee specifically and requiring the level of joined up thinking by the bank – which through a combination over reliance on computer programmes and overseas outsourcing does not always happen.

Fortunately through some fairly hard lobbying by the newspaper the bank accepted their oversight however in conclusion as part of the business sales process make sure the cancellation of personal guarantees are specifically requested and confirmed in writing plus better still existing business bank accounts are closed.

Having a commercial accountant is essential for your business’s financial success. To provide relevant advice it is essential they take an active interest in your business. As a minimum a commercial accountant should

Know business owners as people – what are their personal and business goals, pressures and stresses – both financial and non financial.

Know the business – have they visited your premises, met key employees, understand the business structure, market and your key products and services?

Offer pro-active advice – a commercial accountant should ask questions you have not thought of – for example. Do they bring to your attention future risks and methods to avoid them? Do they offer practical business advice which in the past has been put into practice with positive results? Our industry experience enables us to quickly grasp any root issues and to provide viable solutions leading to savings and efficiencies.

Go the extra mile when you need extra help and support?

All of which are part of the core service offered by the commercial accountants at FD Solutions and Accounting. Using our industry experience our aim is to identify any root issues to then solve problems. We never forget that you the client come first, offering you support in the way you require it.

Here are 10 warning signs to look out for –

Lack of availability – if your accountant is either difficult to get hold of and/or takes a long time to respond it could be a sign you are not considered a priority. Good communication is essential.

Lack of expertise – to provide specific financial advice a truly commercial accountant should have experience relevant to your industry

Little proactive advice – in addition to compliance a good commercial accountant should be looking for opportunities to provide advice to further improve your business performance.

Errors in your financial statements – this could be an indication your accountant is not paying enough attention to detail. Mistakes could cost you money in the long run – its important finding an accountant which is meticulous.

Ethical concerns – if you have any concerns about questionable tax strategies you should distance yourself. If HMRC decide an accountant is doing something dishonest then all their clients could potentially get drawn into the same investigation at significant cost both financially and emotionally to you.

Lack of transparency – your accountant should be transparent about their fees, services and any issues that arise. If you discover any of these not be the case this could be a sign they are not acting in your best interests.

Unresolved issues – if you have raised concerns and these have not been resolved to your satisfaction and/or you do not feel confident in your accountant’s ability to handle your financial needs it’s probably time to look elsewhere.

Lack of innovation – your accountant should be using latest accounting tools and practices, if this is not the case possibly you will be paying for their inefficiencies. An accountant who is not consistently learning and improving their skills may not be able to provide the best service possible.

Incompatibility – if your accountant’s values. work ethic or communication style does not align with yours it could prove difficult to work together effectively.

Business growth – as your business grows your financial requirement will become more complex possibly requiring a higher level of service. It could be that you will need to find a more specialist commercial accountant to support you take your business to the next level.

Changing accountants may be a difficult decision but once made it is fairly quick and easy to do. Remember your financial success depends on having the right professionals defending your corner, someone like FD Solutions and Accounting Limited. We never forget your success is our business!

Employee morale after a holiday season is over is usually low, when your now cash strapped employees return to work with New Year resolutions of asking for a pay rise or worse – ideas of looking for another better paid job! This employee morale focussed tax planning blog explores ways to provide meaningful employee morale boosting rewards that do not result in extra tax liabilities and are fully tax deductible for your company.

Here are some suggestions of tax-friendly methods which equally show appreciation to your team boosting their employee morale –

Idea 1 – £50 gifts – You can give your employees gifts or vouchers up to this amount without their incurring additional tax. Vouchers are convenient and can include those accepted by major online retailers such as Amazon or for food delivery services to treat your team. For non directors there is no annual limit to how much or how many times these are given provided the reason is not performance related, open to all and each time no more than £50.

Idea 2 – Equip their home office – This is a valuable option as you can help create a conducive work environment leading to improved performance and employee morale. Your company will own the equipment, and if they leave, you can reclaim it or sell it to them. Flexible hybrid home working options are now becoming a major factor employees consider when accepting an employment position.

Idea 3 – Provide a mobile phone – Initially, the cost of a phone can be high. This is crucial for employees who have client interactions to separate work and personal life, or for the marketing team to capture high-quality images. Additionally, the monthly contract can be managed through the business without incurring a benefit in kind charge. By covering the cost through the company, you can recover the full expense and VAT. If the employee is expensing the cost, they can only claim for personal use.

Idea 4 – Reimburse home office expenses – Employees can claim certain costs for working from home. If an employee requires a specific broadband service for work, your company can contribute to the business portion. The employee’s work/personal split is 50:50, allowing them to claim 50% through a monthly expense report. In certain cases, flat rate expense claims may be available at £312 per year.

Idea 5 – Branded merchandise – Select an item and add your company’s logo. As long as it’s reasonable and aligns with business needs, it’s tax deductible. T-shirts and sweatshirts are a popular choices.

Idea 6 – Did you forego an office Christmas party? Fear not the tax and national insurance free £150 per employee can be used for any annual event whether this is a late January party, summer event or 2024’s Christmas party – something for everyone to look forward to – boosting employee morale! One other requirement to receive this allowance is that the party must be open to all employees. For those of you with a business operating at multiple sites, HMRC says “If your business has more than one location, an annual event that’s open to all of your staff based at one location still counts as exempt provided it is open to all employees and/or separate parties are held for other locations or departments.

The £150 rule applies to both virtual and in person events.

You may wonder, why should I do this? Well your employees will perceive it as a thoughtful gesture. The VAT is recoverable on direct business purchases and you may also potentially receive up to 25% Corporation Tax relief. Furthermore, branded merchandise offers great exposure for your company. So a win/win for employee morale and your business!

These tax planning strategies not only promote a positive work environment but also address tax considerations. For personalized advice tailored to your business, contact us today and make this a rewarding experience for both your staff and your business.

Manufacturing is a highly innovative UK industry sector in the UK with numerous companies are engaged in activities which meet the criteria for research and development (R&D) tax credits.

However businesses often fail to take advantage of research and development tax relief because they assume that their work is not eligible. While certain forms of commercial product development may not qualify, the manufacturing sector is constantly involved in a wide range of activities and initiatives aimed at advancing knowledge.

Taking the food and drink production sector as an example innovation is necessary as a result of consumer demand, economic pressure (for example cost of living), supply chain or regulatory compliance. Food and drink businesses respond by developing new products to fulfil their preserved market need for example

Improving nutritional benefits

Reduction in salt, sugar, additives

Free-from gluten or particular allergens

Tailored to dietary need (high in protein or fortified in vitamins)

Alcohol free alternatives

Extending shelf life

Addressing sustainability or environmental concerns –

For example eliminating palm oil to protect the Rain Forest

Vegan or organic ranges

Reducing unrecyclable or unnecessary packaging

All product development requires investment and carries a high level of risk. The Research and Development tax credit scheme is a valuable means to help subsidise the cost of such innovation.

To quality a project needs to seek to achieve an advance in science or technology and for these activities to address scientific or technological uncertainty.

When it comes to food and drink products, creating new recipes or formulations is highly likely to fall under Research and Development. The process of innovating and developing these products often involves scientific principles.

Formulating and combining ingredients can introduce uncertainties in their reactions. Even a small change in one ingredient can alter the properties of the mixture and their behaviour in subsequent production stages.

There are also uncertainties in the manufacturing process, such as scaling production, implementing machinery, and establishing processes to ensure a consistent end product.

While meeting consumer expectations for taste, appearance, and unique selling points is crucial, products also need to fulfil various requirements related to shelf life, transportation, compliance with regulations, and affordability.

Utilizing new materials, developing innovative solutions to safety challenges, and integrating new technology can all meet the eligibility criteria. It is crucial for manufacturing companies to monitor their projects and research and development expenses meticulously, as they are required to provide detailed records of the qualifying activities. Seeking professional guidance is essential for a successful tax credit application.

Restaurants and hospitality businesses often overlook the opportunity to claim research and development (R&D) tax credits. Despite ongoing innovation in the form of new processes, services, and recipes, many are unaware of Research and Development tax relief and the activities that could qualify them.

For establishments like restaurants, bars and hotels, investments in delivering better service and advancing methods may be eligible for such credits. This encompasses activities such as creating gluten-free recipes and developing new technology for hotel guests.

Qualifying expenditure includes materials, ingredients, and employee wages related to Research and Development efforts, making expert advice essential in this often disregarded area.

Examples of eligible activities include

The development of vegan and gluten-free alternatives,

Recipe experimentation – including different cooking or food preparation methods

Innovative customer booking apps,

New eco-friendly hotel laundry techniques.

For example, a restaurant successfully improved a signature dish with reduced sugar content after the head chef spent time experimenting with alternative ingredients and preparation methods.

Virtual Finance Directors moving the Finance Department out of the back office shadows to become a true business partner

Used correctly finance business partners are an expensive but valuable resource however in reality very often end up spending much of their time in data manipulation, reconciliations and reports which are of no direct value to a business.

Typically this is a symptom of poor systems and processes but often also due to a lack of understanding as to what activities will drive business value.

Over the last 50 years finance departments have been attempting to change their place in business from merely bean counters – paying the bills and reporting what was happened as a fait-accompli into using this information to become forward looking business decision makers and drivers of performance. This transition continues being a challenging journey since many finance professionals are much happier just crunching numbers rather than becoming involved in commercial interpretation and performance improvement. In recent years improvements to even the most basic of accounting software have both reduced the time finance teams need to spend in data entry whilst offering the ability to report the same information in a variety of different ways with little additional effort – that said as the quality of data improves so has the demand and expectation from other business areas.

I have been involved in rolling out varying aspects of finance department transformation in several businesses and which very often is borne out a necessity for financial information. Typically this request originates from either a Managing Director or their Board of Directors and comes with unrealistic expectation that with additional information and their sudden new found commercial acumen, the quiet finance department will save the business! The latter often being the biggest obstacle to overcome – whilst an effective finance business partner’s commercial acumen should be the number one competency (even above that of bean counting), none the less they are only a voice at the commercial table (albeit influential) but ultimately responsibility should rest with the commercial directors.

Several years ago I worked with a Kent based college group which had acute financial difficulties attributed to poor cost understanding and a lack of individual course profitability analysis based on actual figures. A top level annual budget was being prepared and the finance team were posting invoices to cost centres but further analysis was limited.

Working with each cost centre manager the budget was recalculated by each cost type and significant supplier then into which month the charge would occur. A similar process was introduced for commercial income so turning the budget process onto its head. Monthly meetings to discuss variances and changes to future months were introduced between budget holders and members of the finance team.

Course income was generally funded through central government grants with the amount based on varying student or course criteria. A process for calculating the correct income allocation per course was introduced as an intense annual task. When applied to the costs analysis above provided performance by cost centre and course. In normal circumstances this should have provided the foundation for the finance department to become involved in discussions about curriculum development especially in respect of required course attendance numbers and trends.

Unfortunately in this situation such analysis was left too late. The results just gave meaning to the bank balance that due to insufficient student numbers, courses themselves were either loss making or that this became the case after central management cost had been applied.

Had the finance team become business partners sooner it might have been possible to save this organisation. However this serves to strengthen the potential valuable role finance business partnering can have to a business.

As a summary the key priorities finance heads require to develop a business partnering function are –

Strong and accurate data (which is input in a way that no further reconciliation or sub analysis is required before it can be used for performance reporting)

Finance employees require up skilling in negotiation and influence to underpin their likely analytic ability.

An understanding of Board priority as to where and what suitable analysis and general business support will add value – volume of financial reports is not a guarantee of accepted value.

Many congratulations on your business start-up idea – now the work really begins!

Lets start with a regularly quoted statistic ‘the reason most businesses fail is due to poor financial planning’. We are going to make sure that this is not you through this easy to read blog and Excel templates.

We know even the thought of numbers fills many with dread! Therefore FD Solutions and Accounting are available to answer any of your queries and to assist with your financial and tax returns.

The next sections take you through the various stages of financially planning your start-up business – making sure your business idea is truly financially viable, before you take the plunge.

BUSINESS START-UP EXPENSES

This should be one of the first things you do – even if you discover it is too expensive to start, getting an understanding of costs is important before any financial commitments are made.

It might not be applicable if your business is already started however even then we suggest you complete our spreadsheet including items on hand today (for example cash balances, assets owned etc).

This is one of the few sections of your business plan which won’t be updated (you only start once). Include all expenses involved with starting your business start-up including acquiring a premises, professional insurance, equipment, employee wages and stock/consumables.

If you require funding other than personal savings you’ll need to consider the advantages and disadvantages of each – for example a bank loan could be relatively straightforward but what guarantees are required? Family investment could be another option however would this put strain on relationships at home?

Please email request our accompanying spreadsheet

FINANCIAL PLANNING

The following sections cover vital business start up and ongoing financial planning tools. Once prepared you might require the help of our accountant to explain their meaning or to offer suggestions to keep your business vision on track.

Setting a Sales Price

How do you know how much to sell your products and services for?

This will be decided from market research asking yourself –

How much are your competitors selling a similar product or service?

How does this compare to yours?

Are they offering promotions and packages?

You then need to consider your costs –

What are your direct costs (materials and labour)

How much is it going to cost to produce your product or service?

What are your fixed costs – for example rent, motor vehicles.

Please email request our accompanying spreadsheet

Now you have calculated a selling price you need to decide how customers are going to pay you.

Will it be at point of service

In advance

After the event maybe offering them credit terms

You could consider offering discounts for early payment?

Remember the longer the customer keeps their money the less your business has in its own bank account to use.

Sales Forecast

This is where and when your money is going to come from including plans for growth. It will tell you when you need to employ people or what to do if things do not work out so well.

To complete your sales forecast you need to look back at your vision – how many sales do you need to achieve this?

We suggest you complete at least two sales forecasts – one expected and a second worst case. The worst case then gives time to form a plan should this happen – for example try seeing what happens if you only achieve 50% of year one sales?

Please email request our accompanying spreadsheet

Profit and Loss Projection

This calculates the level of profit you are expecting to produce. It should use the sales totals from your sales forecast combined with the costs directly associated with these sales.

To determine all costs you should consider

Do you need premises to trade from

What purchases (stock to resale/animal feed) do you need to make

Telephone/broadband

Machinery, computer/software licences

Etc

Similar to the sales forecast we suggest you prepare two profit and loss projections – one expected and the other worst case.

Please email request our accompanying spreadsheet

We suggest you prepare a projection for at least five years (then update it on an on-going basis) – as things change so can your projections (for example – win/lose a major client). This is all part of a development plan – development process that develops as your business changes.

This document will be vital if you are applying for a bank loan however even if this is not the case – you need a plan to help fulfil your vision and this is the road map to help you achieve it. We recommend on a monthly basis you look back on these projections and compare them to your actual results – if things have changed update your projections.

For example – if you have not achieved sales targets ask yourself why, is your forecast too unrealistic. What improvement is required for the coming months or is this a permanent?

Cash Flow Forecast

You will no doubt have heard the business comment – cash is king! Never underestimate this, running out of cash (your business life blood) is the most common final reason for business failure – in fact 85% of small businesses start-up fail in the first five years because of cash problems caused by insufficient financial planning – make sure this is not yours!

A cash flow forecast differs to the profit and loss projection as it is based on your business bank balance and when cash is actually received or paid.

This should include

All the cash the business will receive

All the cash the business will pay out

To find this information look at your profit and loss and start up expenses projections. You will need to include cash from any source –

Sales

Money invested by yourself/bank/family etc

Tax refunds

Together with when you are to spend this on, for example

Purchases

Employee wages/your drawings

Motor expenses

Software

Rent

Your accountant!

If you discover your bank account becomes overdrawn you have run out of cash! So time to make alternative plans to prevent this!

Please email request our accompanying spreadsheet

KEEPING FINANCIAL RECORDS

All businesses large or small need to keep financial records both to stay in control of what needs to be paid and to calculate how much tax is owed.

Record keeping does not have to be complex, if you only have a few transactions a spreadsheet should be sufficient.

Please email request our accompanying spreadsheet to get your started.

As your business start up grows there are lots of accounting software packages available some even given free if you hold a business bank account at certain banks. Our recommendation though is Xero Accounting which is cloud based, easily configurable to your business and has many add-ins available (for example banking/payments, ecommerce or time management) in order to adapt as your business grows. It is fast becoming the leading accounting software package used by small/medium sized businesses.

Your will need to register as self employed with HMRC and complete a personal tax return each year. If you are running your business through a company this too needs to register and submit its own tax return – please see the next section for more details.

FINANCIAL YEAR END AND TAXATION

The sort of tax you are liable to pay is dependent on your business structure (for example self employed or a company).

Here is a brief overview of the tax types, how and when to pay them together with sources for additional help.

Corporation Tax – a tax on profits paid by companies

VAT (Value added tax) – a tax on products or services that exceed a turnover of £85,000 a year paid by any applicable business.

Business Rates – a tax on ‘non-domestic properties’ used to run your business paid by the applicable business.

PAYE (pay as you earn) – a tax deducted from salaries paid by any business with employees.

Income Tax – a tax on income (profits) paid by any business

National Insurance – Contributions paid to qualify for a state pension as well as government benefits.

Corporation Tax

Paid by Limited or CIC Companies, clubs, co-operatives and other associates.

This is based on profits and currently at a rate of 19%. From 6th April 2023 this changes to – first £50,000 at 19% and 25% for profits in excess of £250,000. Profits between these amounts will be charged at what is known as a tapered rate equivalent to 26.5%.

Unlike other taxes you will not receive a bill for this. It is up to you to make sure you calculate and submit what you owe to HMRC (or ask for the help of an accountant). You need to apply to the HMRC for a unique tax reference (UTR).

You must always file a company tax return (even if the business makes a loss or does not trade at all).

Filing deadline – 12 months after the end of your accounting period.

Tax payment deadline – 9 months and 1 day after the end of your accounting period. For example – if your company’s year-end is 30th June this will be due on 1st April the following year.

If you are a limited company in your first year of business you may have to file two tax returns. This is because you become incorporated on the day your company is set up but your accounting reference date begins on the last day of the setup month. For example if your company was set up on May 8th, your accounting reference date would not apply until May 31st. Annual accounts cannot cover a period in excess of 12 months two separate returns are necessary to account for the extra 3 weeks.

You can manage taxes yourself but this can be overwhelming especially keeping up to date with changes in legislation (good and bad for businesses). Accountants can help stay compliant and never miss deadlines!

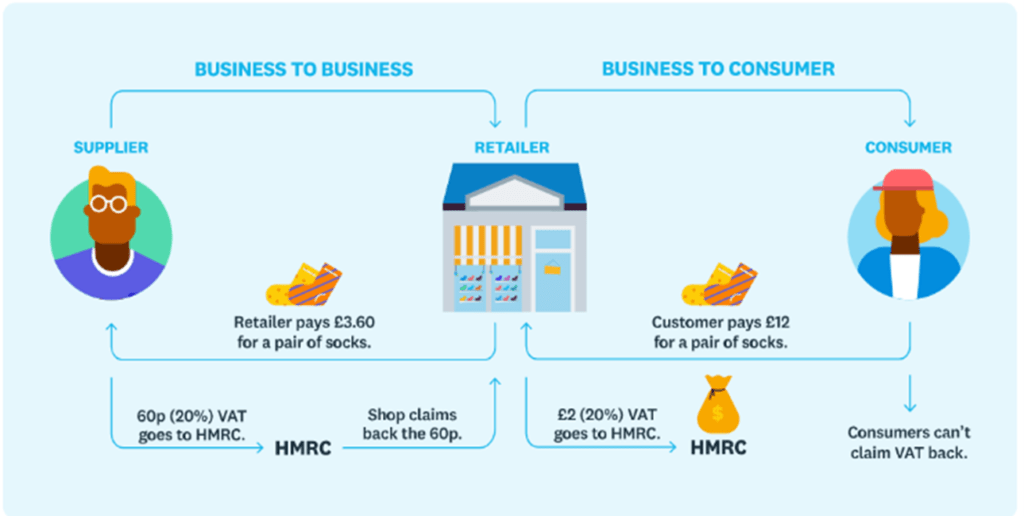

VAT

Value added tax is applicable to businesses with a turnover in excess of £90,000. If your business sells to other businesses (not the public) it is possible to register below this threshold.

VAT is added to every item you sell (at 20%).

When the buyer makes a purchase from a supplier this is called input tax and when a customer makes a purchase from a buyer this is known as output tax.

Businesses registered for VAT must submit (typically quarterly) to the HMRC details of VAT they’ve charged and paid. If they have paid more than charged HMRC will refund the difference otherwise they will need to pay what is owed. This submission has to be submitted digitally from within accounting software (our recommendation is Xero).

The standard VAT rate is 20% but some products and services are subject to lower rates or exempt/zero rated (for example water, most food or children’s cloths).

Please email to request our worksheet to help you decide if you should register for VAT.

HMRC offer a simplified process for businesses with a turnover below £150,000 known as the Flat Rate Scheme. Please ask FD Solutions and Accounting for further details.

Business Rates

You will need to pay business rates if you use any ‘non-domestic properties’ to run your business – this can include a home office.

Business rates are typically paid monthly with annual bill arriving in February or March of each year.

PAYE

If you have employees you are responsible for the PAYE tax (pay as you earn). This is an income tax which is deducted from salaries. These salaries include employees and your own (if your business is a company) and any other director.

You will need to register your business for PAYE with HMRC.

Income Tax rates and bands (frozen until 2028) are

Band

Taxable Income

Tax Rate

Personal allowance

Up to £12,570

0%

Basic rate

£12,571 to £50,270

20%

Higher rate

£50,271 to £150,000

40%

Additional rate

Over £150,000

45%

If you pay employees monthly you must pay their deductions to HMRC by 22nd of the following tax month.

If you pay quarterly you must pay their deductions to HMRC by 22nd of the month following this quarter.

Payroll submissions must be made digitally from within accounting software (our recommendation is Xero).

If you are employing people please be aware of legislation regarding minimum wage, hours and legality to work.

Income Tax

Simply put – this is a tax on income. This is payable on any income earnt as a sole trader, director or partner.

In addition to salary this also covers –

Self-employed profits

State benefits

Pensions

Rental Income (above rent a room scheme)

Trust income

Income on savings (in excess of allowance)

You’ll need to pay your income tax with self assessment by 31st January.

National Insurance

You’ll need to pay National Insurance to qualify for a state pension as well as various government benefits.

Anybody aged over 16 must pay NIC if they are self-employed and making profits in excess of £12,570 or earning more than £241 per week.

National Insurance classes range from 1-4. The type of class you pay varies by employment status, income and whether or not you employ people.

Employed

2024-25 National Insurance

How much you earn

Class 1 Rate

Less than £12,570

0%

£12,570 – £50,270

12%

More than £50,270

2%

Self employed

How much you earn

Class 2 and 4 rates

Less than £6,725

0%

£6,725 – £12,570

£3.45 per week

£12,570 – £50,270

6.00% + £3.45 per week

More than £50,270

2.00% + £3.45 per week

If you are self-employed there are different classes you may fall under

Self-employed: Sole traders must pay Class 2 and Class 4 NIC

Self-employed and employed: Limited company directors who are their own employees must pay Class 1 NICs

As a director you pay NICs through your own PAYE payroll and sole traders must include their contribution in their annual self-assessment.

Which tax type applies to my business?

Sole trader and Partnerships (including LLPs)

Sole traders pay Income Tax on any taxable profits. This is done on an annual basis as part of your self assessment.

For 2024/25 the tax free personal allowance is £12,570 meaning you will not pay income tax until you earn anything beyond that threshold.

Your tax rate also depends on your total annual profit and is distributed as follows –

Basic rate – 20% on profits between £12,571 and £50,270

Higher Rate – 40% between £50,271 and £150,000.

Additional Rate – 45% on profit in excess of £150,001

You must also pay NICs which is a Class 2 flat rate for any profits above £6,725 per annum together with 9% Class 4 if your profits are between £12,570 and £50,270.

Private Limited Company (including CICs)

All companies must pay Corporation Tax on any profits at 19% for the first £50,000 of profits.

There are certain reliefs which can reduce your bill – for example

Claiming research and development relief (R&D) or capital allowances for equipment purchases. For further details please speak to us.

Directors can also pay themselves a dividends (if the company has made a profit). For tax year 2024/25 the first £500 is tax free then – basic rate taxpayers pay 8.75% on dividends, higher rate-taxpayers 33.75% and additional-rate taxpayers 39.35%. There are often tax advantages to taking dividends in lieu of a salary – please ask our accountant for more details.

A positive result for this business. The article below demonstrates a common tactic used by HMRC in visiting the establishment as a secret customer and observing – the restaurant/fast food sector is a soft, easy target for HMRC. Another common strategy HMRC use is to visit a restaurant as a diner and leave a tip then audit its treatment during an inspection … sneaky. We are aware of these and other tricks – make sure you stay protected and tax compliant!

Not a sweet outcome for Mcvities this time with HMRC. Having successfully argued Jaffa cakes should be VAT free some years ago McVities luck ran out in the latest challenge – which though it pains me saying it was a fair outcome for HMRC!

Similar to the infamous Jaffa Cakes case, this too focused on the interpretation of the VATA 1994 Section 30 – which states food should be zero rated unless its “confectionery, not including cakes or biscuits other than biscuits wholly or partly covered with chocolate or some product similar in taste and appearance”.

The Blissfuls case centred on whether the chocolate covered or filled the biscuits – which the tribunal ruled we covered and so subject to VAT.