Before proceeding further I believe Tim Meadows-Smith is explaining the role of a Financial Controller, very much a business defender ensuring tax and legislative compliance together with accurate historical reporting – never strategic but a firm base for a finance director/CEO to start their projections.

There is however very much more of a risk for smaller businesses which do not require a full time finance director but need more than just their year end accounts. Often at this point in their business journey, owners realise the need and either reach out to a business coach or to their external accountants who both claim they can assist.

Business Coach scenario

The business coaches love an ambitious business owner and will encourage them to put together a three to five year business and personal plan based on their dreams.

The coach then sets regular goals, however nobody is looking at whether there is sufficient cash available to fund the targets or checking the actual profitability of the new business.

12 months later the business either folds due to a lack of cash, else their external accountants are employed to assist in mopping up the mess. This often includes having spent up to a six figure sum for this ‘advice’.

External High Street Accountants Scenario

As the preparer of their year end accounts and tax returns these are often the obvious first choice of professional which quite rightly the SME business owner speaks. Unfortunately most High Street accountants believe they have the skills to assist – which in theory is correct however they lack practical experience of ever properly working in a business (at best sitting in a closed door board room, whilst carrying out an audit), meaning anything offered is theoretic and very much leaning towards historic analysis rather than working beside the CEO, providing the financial case for chasing new contracts together with their impact to EBITDA and the cash position.

Result – the business stumbles on with some improved reporting, possibly monthly management accounts which report line of business profitability and a 12-month forecast, however lacking the spontaneity to spot opportunities, and asking the questions that drive real decisions such as –

What’s the expected cash balance in 90 days?

What is the profitability by product line and does it cover overheads?

Which parts of the business are actually making money?

Can we afford to recruit – and when?

If nobody in a business is asking those questions, they are flying blind.

Solution – for an ideal fractional finance director

Recruit either a full or part time fractional finance director which has been industry trained. Having obtained their financial experience whilst working in a business means they have a greater chance to properly identify drivers of performance and instinctively to understand and to analyse operations. Typically 90% of their work is forward looking – typically using monthly management accounts which split income streams by profitability as a base.

Typically the best fractional finance directors are business leaders which just happen to also be in charge of finance. They are strategic thinkers who are able to identify opportunities together with adding financial confidence to board proposals.

Practice accountants struggle with fractional finance director positions because of the vast difference in the skillset required to carry out the position. Whilst many practice accountants are highly technical they struggle with the ‘big picture’ business strategy together with the company board leadership skills required of a finance director position.

Here is a summary of the key reasons why this transition can be challenging

Reactive, backward looking perspective

Practice trained accountants are mainly focused on historic data – compliance, tax returns or in auditing its accuracy.

For a fractional finance director it is essential they are forward looking – whether this is modelling future performance or anticipating future business needs. Practice accountants often struggle with this falling back to prioritising analysing the past.

Lack of a commercial mindset

Cost v Value – practice accountants are trained to be risk adverse and to focus on cost cutting

Commercial Reality – A successful fractional finance director acts as a business partner understanding how to drive revenue, increase value and to support growth – not just how to manage expenses.

Weak operational and/or strategic focus

Technical v Operational – as a consequence of the only true business work experience being audit related visits, practice accountants generally lack experience in operational management such as supply chain, human resources or marketing – so critical to a CEO’s strategic vision.

Over-reliance on Numbers – Practice accountants tend to become too involved in technical accounting details and fail to look at the ‘big business picture’.

Limited leadership and communication skills

Communication Gaps – Practice accountants are often weak in translating complex financial data into actionable insights for non-financial employees – which is so key for effective leadership.

‘Policing’ Mindset – instead of aiming to develop and empower the wider organisation some accountants will focus too much on enforcing strict, bureaucratic procedures.

Risk-averse nature

Caution – due to practice training being very much focused on preventing errors and fraud, they can be overly conservative so hindering growth in high paced or entrepreneurial businesses.

Lower Strategic Impact – Research suggests accountants with a strict auditing background may not be effective in high-growth industries which require bold, strategic investments.

Differences Summary

Aspect

Practice Accountant

Finance Director (Industry)

Focus

Past, historic and compliance

Future, strategic and proactive

Viewpoint

Technical and detail-orientated

Commercial and strategic

Role

Cost-centre management

Revenue and value generation

Approach

Risk averse

Risk Managed/calculated risk

While these are common challenges it is possible for a practice accountant to succeed as a finance director/CFO if they are able to develop a commercial mindset, improve communication and to shift their focus from compliance to business growth.

You have a bookkeeper or a small accounts team responsible for ensuring that your customers are paying you, and that suppliers and payroll payments are made when they are due.

At the end of each financial year, an accountancy firm prepares your annual financial statements and submits your tax returns.

On a daily basis, you lack financial transparency, which is impacting your business growth and causing sleepless nights.

Your business might not be big enough to justify the necessity (and expense) of hiring a full-time virtual CFO, but…

Is it time to find a part-time virtual CFO?

A virtual CFO could provide the clarity, direction, and financial credibility you are looking for. If affordability is a concern, the cost-effective nature of a part-time virtual CFO might surprise you. You can access senior-level financial expertise without the commitment or expense of a full-time employee.

This forward looking service is so new that the job market has yet to decide on a title. The same position is known as either –

Outsourced Finance Director

Virtual Finance Director

Fractional Finance Director

Virtual CFO

Fractional CFO etc

However the services and benefits are similar –

Financial Clarity

You have aspirations, whether it’s to expand, secure funding, sell, or simply become more profitable. To achieve these goals, you require comprehensive financial insights to guide your decisions.

Without this information, it’s challenging to identify your most profitable customers or products and determine the areas for potential growth.

Setting a realistic yet challenging budget involves more than a vague 10% increase estimate. It requires a detailed understanding to gain your team’s support and ensure accountability in achieving targets.

Predicting cash flow fluctuations in the upcoming months is crucial to avoid running out of funds, especially when expenses like VAT payments are due. A Part-Time Virtual CFO can assist in creating budgets, cash flow forecasts, client profitability reports, and management accounts, providing valuable insights and expert analysis to help you make informed decisions.

More time for you to do what you went into business to do.

Having a skilled virtual CFO on your team allows you to focus on your core abilities and advancing your business – the tasks you envisioned when starting your business. Additionally, you will be more well-informed.

Better decision making

A virtual CFO can provide valuable financial knowledge and insight to help you make informed decisions. Serving as your trusted advisor, the Part-Time virtual CFO will support your strategies, offer valuable feedback, and maintain impartiality with your best interests at heart.

Enhanced relationships

Having a financial expert with a strong reputation in your company can enhance your financial standing with banks, investors, auditors, and insurers, potentially leading to new opportunities. Allow your virtual CFO to handle negotiations and bolster connections with stakeholders.

Flexible and cost effective

Receive financial expertise and strategic advice at the board level for your business without the expenses and obligations associated with hiring a full-time CFO.. You only pay a day rate for the days you require. Additionally, a virtual CFO can provide flexibility by adjusting the time dedicated to you during crucial projects.

About FD Solutions and Accounting

FD Solutions and Accounting provide virtual CFOs to growing and ambitious small and medium businesses in South East England with a typical turnover in excess of £100K. Typically we spend between 5-15 hours per week working with each client through a mixture of remote and on-site.

Hiring a part-time virtual CFO can provide your business with the expertise and practical knowledge to take it to its next stage, whether through organic growth, acquisition, securing funding, private equity or preparing for an exit strategy. You do not need to hire a full time CFO to receive the benefits of one.

Straight talking with an objective of making businesses more financially aware our dynamic approach sets us apart.

Excellent news for Kent and Medway based businesses…

Kent and Medway business fund is now accepting applications for 0% loans between £25K – £99K from small and medium sized business start-ups to help develop new and expand existing products, services or processes which in turn can create jobs, drive growth and improve productivity.

Could be this expenditure will quality for generous R&D tax credits too!!!.

Key eligibility requirements

Your business must be able to prove a good profitable track record

Be creating or protecting sustainable jobs

Must not be subject to collections or insolvency proceedings.

Any funding must be 20-30% match funded via business reserves or bank loans.

Please note depending on assessed risk at the discretion of the council further personal security may be required.

Established businesses or those seeking a larger loan can apply for a KMBF Standard loan.

Finer details about both loans and how to apply can be found at

A word of caution when selling your business which contains personal guarantees for the business loans or overdrafts.

A case was reported in the financial press recently where a business owner had sold their business and duly informed their bank of the sale and their desire to be removed from the bank account as they were no longer a director providing the new owner details at the same time. Role forward 18 months and the bank are demanding the old owner repay an overdraft of almost £40K racked up by the new owner who has also filed for insolvency….

The mistake the former owner appears to have made was not asking the bank to remove their personal guarantee specifically and requiring the level of joined up thinking by the bank – which through a combination over reliance on computer programmes and overseas outsourcing does not always happen.

Fortunately through some fairly hard lobbying by the newspaper the bank accepted their oversight however in conclusion as part of the business sales process make sure the cancellation of personal guarantees are specifically requested and confirmed in writing plus better still existing business bank accounts are closed.

Farm Accountant FD Solutions and Accounting believe that a mixture of both economic and financial pressures are forcing farmers to diversify their income streams to support their businesses long term.

Engaging professional support in the feasibility stages maximises the chances of developing proposals which will secure the bank funding needed. Here are five areas worth consideration in the planning stage.

Diversification

With so many options available, farm accountants FD Solutions and Accounting believe what works for one farm might not be possible for another. Always keep in mind whether this income stream will achieve desired end aims and whether this produces –

Cashflow to support existing lines of business.

Employment or a business opportunity for family or staff members

Capital growth

Better use of assets

It is always preferable to consider more than one investment opportunity so as to weigh up each’s strengths and weaknesses against original objectives.

Return on Investment

Alongside the usual financial KPI measure, we believe certain non-financial matters could be equally as important, such as –

Can the existing business still run with management’s time diverted to this potential project.

How will this impact existing staff – who typically bear the impact of change.

Is it possible to assess what additional skills (or training) will be required.

How resilient do you consider yourself and have you planned for unforeseen issues?

Professional Advice

Farm accountants FD Solutions and Accounting consider engaging professional advice during the planning stage is key. This could be a fractional finance director / CFO, solicitor or land agent together with family members. Typically lenders will be looking to satisfy themselves that –

Any planning permission has been received

Any renovation or new build has been costed and competitively quoted.

Does any funding request adequately cover project timescales with adequate contingencies

Are relevant licences in place

What corporate structure will the new venture take – for example limited company.

Business Plan

A good business plan should provide confidence to you, family and lenders. Farm accountants FD Solutions and Accounting recommend you identify areas to focus on and that risks are properly accounted for.

This should include a summary covering what is planned, funding requirement along with the payback period. The main plan ought to include –

What makes the venture unique or different

Local competition

Evidence of a customer demand. This could come from, for example research or test trading

Route to market and why – for example social media, content and platform.

Are the financial projections expected – if they look too good the lender will most certainly question them!

Assumptions and research to underpin financial projections

Budget projections for different scenarios – best, worst and most likely.

Reasonable repair costs to keep the project ‘like new’

Is the cash conversion cycle reasonable – no good having profits tied up for long periods as production costs or trade debtors. Cash makes loan repayments not profit!

What the Lender Wants

From FD Solutions and Accounting experience with farm accounting expect a Dragon’s Den type of challenge to your figures. Lenders require confidence every aspect of your investment stands up and that a business plans shows –

A proposition which is well considered and researched

Balanced funding proposal clearly defining your stake in the new venture

Contingency plan scenarios if business levels are not achieved.

Route to repayment of the lenders funding together with a timescale

FD Solutions and Accounting has many years of experience preparing business plans and understand the importance of future investment. We are committed to helping our farming customers turn their plans into success. We are based in Paddock Wood, West Kent and have clients throughout the county, in East Sussex and nationally.

Employing the right people in your team is essential for business success. You need an expert who can make sure everything runs smoothly and that’s where a modern part-time fractional CFO comes in. A modern fractional CFO is invaluable to all businesses regardless of their size, complexity or market for the following reasons –

Use of accurate information for data-driven decisions

The modern fractional CFO oversees data from all areas of the business ensuring this is both accurate and up to date. This is used to provide informed advice on how to proceed with any investment, operation or other strategic initiative within the business.

Ability to adapt

Technology, regulation and laws – especially around your business operations are continually evolving or changing. It is the role of a fractional CFO to both remain up to date in all and to ensure their compliance or application has the best possible outcome for the business. Most recent emergences have been in cloud computing, automation and AI aiding efficiencies in routine tasks and capabilities in management reporting and analysis set against the challenges of home working and cyber security.

This said systems, controls and the level of information needs to be appropriate for the size of the company – ideally with scalability factored in. This needs to be suitable for its intended readers – i.e. senior leadership team, shareholders, executive committee and employees.

There are many MDs which do not completely understand their accounts but feel (incorrectly) reassured by graphs and charts – too much information is as bad as not enough. The best reporting in the world is worthless if its message is not understood!

Maximising Profits

An effective fractional CFO will audit current costs and identify potential areas for cost savings and efficiencies. They also help develop plans for future budgeting and forecasting activities so the business is always aware of their financial outlook ahead of time. A budget is used as a yardstick to compare against actual performance (good or bad), the results of which being used for future forecasts and planning.

Improving Compliance

The modern fractional CFO ensures compliance with accountancy rules and ensures submissions to HMRC and Companies House are both accurate and timely. They keep track of changes in legislation together with compliance with existing rules. This reduces the risk of future fines due to non-compliance issues.

Bringing out the best in the in-house bookkeeping team

A fractional CFO will develop, motivate and provide direction to your in-house bookkeeping team. This will be achieved through setting goals, targets and priorities so ensuring transactions are accurately processed competently performing routine tasks so ensuring reporting is timely and accurate – a true aid to decision making.

The glue to hold other areas of the business together

The fractional CFO’s ability to read business information should enable them to use this to drive informed change. They should be ‘critical friends’ with all areas of the business challenging managers to provide ‘cost-benefit’ for any expenditure or investment purchase done without affecting the ability of the company to carry out its underlying strategy.

Having a modern finance director as part of your team can be invaluable when it comes to maximising profits, improving compliance, and making data-driven decisions within your business – no matter its size! Not only do they provide expertise in various financial matters but they also act as a valuable resource for generating new ideas and strategies for taking your business into different areas.

A modern fractional CFO is invaluable to all businesses regardless of their size, complexity or market. Our flexible tailored packages start from one day per month making this service truly available to all. This is a core specialism of FD Solutions and Accounting please contact us for more information and to discuss our flexible packages.

Virtual Finance Directors moving the Finance Department out of the back office shadows to become a true business partner

Used correctly finance business partners are an expensive but valuable resource however in reality very often end up spending much of their time in data manipulation, reconciliations and reports which are of no direct value to a business.

Typically this is a symptom of poor systems and processes but often also due to a lack of understanding as to what activities will drive business value.

Over the last 50 years finance departments have been attempting to change their place in business from merely bean counters – paying the bills and reporting what was happened as a fait-accompli into using this information to become forward looking business decision makers and drivers of performance. This transition continues being a challenging journey since many finance professionals are much happier just crunching numbers rather than becoming involved in commercial interpretation and performance improvement. In recent years improvements to even the most basic of accounting software have both reduced the time finance teams need to spend in data entry whilst offering the ability to report the same information in a variety of different ways with little additional effort – that said as the quality of data improves so has the demand and expectation from other business areas.

I have been involved in rolling out varying aspects of finance department transformation in several businesses and which very often is borne out a necessity for financial information. Typically this request originates from either a Managing Director or their Board of Directors and comes with unrealistic expectation that with additional information and their sudden new found commercial acumen, the quiet finance department will save the business! The latter often being the biggest obstacle to overcome – whilst an effective finance business partner’s commercial acumen should be the number one competency (even above that of bean counting), none the less they are only a voice at the commercial table (albeit influential) but ultimately responsibility should rest with the commercial directors.

Several years ago I worked with a Kent based college group which had acute financial difficulties attributed to poor cost understanding and a lack of individual course profitability analysis based on actual figures. A top level annual budget was being prepared and the finance team were posting invoices to cost centres but further analysis was limited.

Working with each cost centre manager the budget was recalculated by each cost type and significant supplier then into which month the charge would occur. A similar process was introduced for commercial income so turning the budget process onto its head. Monthly meetings to discuss variances and changes to future months were introduced between budget holders and members of the finance team.

Course income was generally funded through central government grants with the amount based on varying student or course criteria. A process for calculating the correct income allocation per course was introduced as an intense annual task. When applied to the costs analysis above provided performance by cost centre and course. In normal circumstances this should have provided the foundation for the finance department to become involved in discussions about curriculum development especially in respect of required course attendance numbers and trends.

Unfortunately in this situation such analysis was left too late. The results just gave meaning to the bank balance that due to insufficient student numbers, courses themselves were either loss making or that this became the case after central management cost had been applied.

Had the finance team become business partners sooner it might have been possible to save this organisation. However this serves to strengthen the potential valuable role finance business partnering can have to a business.

As a summary the key priorities finance heads require to develop a business partnering function are –

Strong and accurate data (which is input in a way that no further reconciliation or sub analysis is required before it can be used for performance reporting)

Finance employees require up skilling in negotiation and influence to underpin their likely analytic ability.

An understanding of Board priority as to where and what suitable analysis and general business support will add value – volume of financial reports is not a guarantee of accepted value.

Profit margin can be increased by at least 5% with the assistance of a Virtual CFO – here is an example of how we’ve helped a past client, not solely consultancy but hands on delivery.

Case Study

At £5 per £100 5% does not sound much however a £3 million saving per £60 million of sales and this starts looking worthwhile! Even better, whilst some of the improvements listed below helped me achieve this increase, in businesses where these have been completely overlooked the savings could be much more significant!

Gross profit margin is the profit percentage of sales less direct costs of manufacture, for example materials and the wages of the production team. Some organisations, where it can be attributed directly to production or distribution also include the manufacturing element of utilities and motor vehicle costs.

I achieved this success whilst working as an international virtual CFO for fine food distributor Classic Fine Foods then trading in a dozen Asian countries. The Group sales at the time was £60m and my annual savings amounted to £3m.

As a distributor to a crowded market often with exclusive selling agreements for many of the products there was little manoeuvrability on sales price so any improvements had to be achieved from cost, process efficiency or sales volume.

Savings achieved

Using a report written from the accounting system – profitability analysis of every transaction by both product and customer was produced. This identified poorly performing products and customer buying patterns plus over reliance to either. Products not achieving a desired gross profit margin and not deemed to be loss leaders were discontinued. From a monthly customer buying analysis it was possible to pick up patterns and trends. The variations were passed to the sales team to discuss with the customer resulting in both additional sales and warnings of potential quality issues.

Inventory management – through the introduction of real time stock reports it was possible to both identify slow moving product lines and to track product expiry dates (critical for perishable items). Both of these were previously being managed through manual processes. The result was a reduced amount of product requiring promotional discount pricing as a result of short storage life and the phasing out of slow moving product lines – so freeing both working capital and storage space for faster stock turnover item lines.

Stock write offs were analysed and product quality issues established either generally or customer specific, through addressing the root issue these were significantly reduced.

Prior to real-time automated stock reporting some information was being prepared manually, duplicating data entry. This employee time saving was estimated to be approximately two days a week per business location.

Other factors which will affect a sales gross margin to be aware of, but not applicable to my case study above are –

Product theft – beware of excessive product write off or stock count differences between physical and computer system amounts.

Excessive product wastage in a production process – this could indicate poor product quantity, inefficient production process or worst case inaccurate product costing..

Are price changes for materials or substitutions being regularly updated in costings schedules then reflected in the customer selling price lists.

Minimum sales order value – regardless of its value its highly likely the cost of order processing and delivery (if a van drop-off service is provided) will cost the same amount.

Excessive customer discounting. Businesses offer sales discounts in the hope their customers will buy more – so boosting the part of the gross profit margin foregone. Often this does not happen. This is best explained with an example – If a product costs £70 and the selling price is £100 the gross profit will be £30 (or 30%). If the selling price is reduced by 10% to £90 the gross profit reduces to £20 (or 22%) so the business now has to sell 50% more to achieve the same profit margin position.

In reality sales discounts are most likely to be 20-25% – i.e. goods almost sold at cost!

However work this in reverse in conjunction with a marketing campaign about product quality and sales prices could be increased by 10% to £110 so producing a 33% increase in gross profit margin for just a 10% increase in selling price!

Warranty claims – either the labour cost of a repair or a product replacement will be a cost without any additional income – unless there are guarantees which can be recharged to the source supplier.

In conclusion the factors which have a direct effect to an expected gross profit margin are –

Misunderstood product pricing or the production costs to manufacture

Well lets re-phase this – what are the key factors potential buyers will be looking at when acquiring your business – each of which adding a premium to the asking price. Achieving these is no overnight fix and only come from focus and planning, however will offer your business resilience ready for whenever you plan to sell it.

Value Driver 1 – A Predictable and Consistent Cash Flow

Sales turnover and a positive cash flow will be one of the first business areas a buyer looks at. Established growth patterns carry a premium which will be higher depending on the level of recurring sales. This demonstrates a level of stability and a lower risk of being lost with a transfer of ownership. Examples of recurring sales are maintenance contracts, subscriptions or service agreements/warranties. Buyers are willing to pay the highest amount when they feel a positive cash flow is predictable and repeatable.

Value Driver 2 – Broadness of the Customer and Product sales base

Aim at ensuring no single customer or product makes up more than 10% of total sales. This helps to protect the business from a loss of a significant customer or product and the cash impact this will cause. Ideally products should be sold to multiple market sectors too.

Value Driver 3 – Reliable Financial Information

Goes without saying reliable financial records are critical for ongoing business management which in the company sale process can be used by the buyer to carry out due diligence to have proof of the figures. Any level of doubt will have a negative impact to the purchase price.

Value Driver 4 – Quality of the Employees

Employees should be a business’ greatest asset. Developing a low employee turnover ensures experience and depth of knowledge together with less time spent with recruitment (and its associated costs) and newbee training. An in-place team will provide continuity and assist with business growth under any new ownership and as such are a desirable asset.

Value Driver 5 – Potential future Growth

At least annually a business should prepare a sales forecast and business plan for the coming year on which actual performance should be assessed. The sales forecast should be derived from a growth plan which identifies realistic opportunities and profit. Such a plan will be of significant value to a buyer which might identify areas they had not considered. Areas to consider in a growth plan

If the business in a growth industry are there additional markets to pursue

What existing products could be sold to existing customers

Which products make the best profit margins – how can their sales be increased or margins replicated in other product lines?

Are there technology licencing or product franchising opportunities

Value Driver 6 – Operating Systems and Procedures

Documented standard business procedures and systems help ensure product quality and aid employee learning in how the product is delivered. This enables continuity under any new ownership. The following are examples of business systems which enhance value –

Employee recruitment, training and retention

Product development and improvement

Product quality control

Business or product certification (for example ISO 9001/14001 or 18001)

Employee manual

Customer, supplier and employee communication

Value Driver 7 – Facility and Equipment Condition

Well maintained, tidy and modern facilities & equipment are not only likely provide the lower overhead running costs but also to realise a higher business sale value. Potential buyers will be put off by poorly maintained equipment and facilities perceiving other aspects of the business may be similarly disorganised. Buyers will also be looking for a modest amount of space capacity to accommodate some sales growth.

Value Driver 8 – Barriers to Entry

Businesses should look at how they can protect themselves from competitors to strengthen its strategic position – their effectiveness of this adds a premium to a business sales price such as –

Aside trademarks, patients or hard to get licences

Trade secrets

Developed processes and propriety know-how

Hard to get contracts (for example government)

Goodwill – brand name, customer awareness or a good reputation.

Many congratulations on your business start-up idea – now the work really begins!

Lets start with a regularly quoted statistic ‘the reason most businesses fail is due to poor financial planning’. We are going to make sure that this is not you through this easy to read blog and Excel templates.

We know even the thought of numbers fills many with dread! Therefore FD Solutions and Accounting are available to answer any of your queries and to assist with your financial and tax returns.

The next sections take you through the various stages of financially planning your start-up business – making sure your business idea is truly financially viable, before you take the plunge.

BUSINESS START-UP EXPENSES

This should be one of the first things you do – even if you discover it is too expensive to start, getting an understanding of costs is important before any financial commitments are made.

It might not be applicable if your business is already started however even then we suggest you complete our spreadsheet including items on hand today (for example cash balances, assets owned etc).

This is one of the few sections of your business plan which won’t be updated (you only start once). Include all expenses involved with starting your business start-up including acquiring a premises, professional insurance, equipment, employee wages and stock/consumables.

If you require funding other than personal savings you’ll need to consider the advantages and disadvantages of each – for example a bank loan could be relatively straightforward but what guarantees are required? Family investment could be another option however would this put strain on relationships at home?

Please email request our accompanying spreadsheet

FINANCIAL PLANNING

The following sections cover vital business start up and ongoing financial planning tools. Once prepared you might require the help of our accountant to explain their meaning or to offer suggestions to keep your business vision on track.

Setting a Sales Price

How do you know how much to sell your products and services for?

This will be decided from market research asking yourself –

How much are your competitors selling a similar product or service?

How does this compare to yours?

Are they offering promotions and packages?

You then need to consider your costs –

What are your direct costs (materials and labour)

How much is it going to cost to produce your product or service?

What are your fixed costs – for example rent, motor vehicles.

Please email request our accompanying spreadsheet

Now you have calculated a selling price you need to decide how customers are going to pay you.

Will it be at point of service

In advance

After the event maybe offering them credit terms

You could consider offering discounts for early payment?

Remember the longer the customer keeps their money the less your business has in its own bank account to use.

Sales Forecast

This is where and when your money is going to come from including plans for growth. It will tell you when you need to employ people or what to do if things do not work out so well.

To complete your sales forecast you need to look back at your vision – how many sales do you need to achieve this?

We suggest you complete at least two sales forecasts – one expected and a second worst case. The worst case then gives time to form a plan should this happen – for example try seeing what happens if you only achieve 50% of year one sales?

Please email request our accompanying spreadsheet

Profit and Loss Projection

This calculates the level of profit you are expecting to produce. It should use the sales totals from your sales forecast combined with the costs directly associated with these sales.

To determine all costs you should consider

Do you need premises to trade from

What purchases (stock to resale/animal feed) do you need to make

Telephone/broadband

Machinery, computer/software licences

Etc

Similar to the sales forecast we suggest you prepare two profit and loss projections – one expected and the other worst case.

Please email request our accompanying spreadsheet

We suggest you prepare a projection for at least five years (then update it on an on-going basis) – as things change so can your projections (for example – win/lose a major client). This is all part of a development plan – development process that develops as your business changes.

This document will be vital if you are applying for a bank loan however even if this is not the case – you need a plan to help fulfil your vision and this is the road map to help you achieve it. We recommend on a monthly basis you look back on these projections and compare them to your actual results – if things have changed update your projections.

For example – if you have not achieved sales targets ask yourself why, is your forecast too unrealistic. What improvement is required for the coming months or is this a permanent?

Cash Flow Forecast

You will no doubt have heard the business comment – cash is king! Never underestimate this, running out of cash (your business life blood) is the most common final reason for business failure – in fact 85% of small businesses start-up fail in the first five years because of cash problems caused by insufficient financial planning – make sure this is not yours!

A cash flow forecast differs to the profit and loss projection as it is based on your business bank balance and when cash is actually received or paid.

This should include

All the cash the business will receive

All the cash the business will pay out

To find this information look at your profit and loss and start up expenses projections. You will need to include cash from any source –

Sales

Money invested by yourself/bank/family etc

Tax refunds

Together with when you are to spend this on, for example

Purchases

Employee wages/your drawings

Motor expenses

Software

Rent

Your accountant!

If you discover your bank account becomes overdrawn you have run out of cash! So time to make alternative plans to prevent this!

Please email request our accompanying spreadsheet

KEEPING FINANCIAL RECORDS

All businesses large or small need to keep financial records both to stay in control of what needs to be paid and to calculate how much tax is owed.

Record keeping does not have to be complex, if you only have a few transactions a spreadsheet should be sufficient.

Please email request our accompanying spreadsheet to get your started.

As your business start up grows there are lots of accounting software packages available some even given free if you hold a business bank account at certain banks. Our recommendation though is Xero Accounting which is cloud based, easily configurable to your business and has many add-ins available (for example banking/payments, ecommerce or time management) in order to adapt as your business grows. It is fast becoming the leading accounting software package used by small/medium sized businesses.

Your will need to register as self employed with HMRC and complete a personal tax return each year. If you are running your business through a company this too needs to register and submit its own tax return – please see the next section for more details.

FINANCIAL YEAR END AND TAXATION

The sort of tax you are liable to pay is dependent on your business structure (for example self employed or a company).

Here is a brief overview of the tax types, how and when to pay them together with sources for additional help.

Corporation Tax – a tax on profits paid by companies

VAT (Value added tax) – a tax on products or services that exceed a turnover of £85,000 a year paid by any applicable business.

Business Rates – a tax on ‘non-domestic properties’ used to run your business paid by the applicable business.

PAYE (pay as you earn) – a tax deducted from salaries paid by any business with employees.

Income Tax – a tax on income (profits) paid by any business

National Insurance – Contributions paid to qualify for a state pension as well as government benefits.

Corporation Tax

Paid by Limited or CIC Companies, clubs, co-operatives and other associates.

This is based on profits and currently at a rate of 19%. From 6th April 2023 this changes to – first £50,000 at 19% and 25% for profits in excess of £250,000. Profits between these amounts will be charged at what is known as a tapered rate equivalent to 26.5%.

Unlike other taxes you will not receive a bill for this. It is up to you to make sure you calculate and submit what you owe to HMRC (or ask for the help of an accountant). You need to apply to the HMRC for a unique tax reference (UTR).

You must always file a company tax return (even if the business makes a loss or does not trade at all).

Filing deadline – 12 months after the end of your accounting period.

Tax payment deadline – 9 months and 1 day after the end of your accounting period. For example – if your company’s year-end is 30th June this will be due on 1st April the following year.

If you are a limited company in your first year of business you may have to file two tax returns. This is because you become incorporated on the day your company is set up but your accounting reference date begins on the last day of the setup month. For example if your company was set up on May 8th, your accounting reference date would not apply until May 31st. Annual accounts cannot cover a period in excess of 12 months two separate returns are necessary to account for the extra 3 weeks.

You can manage taxes yourself but this can be overwhelming especially keeping up to date with changes in legislation (good and bad for businesses). Accountants can help stay compliant and never miss deadlines!

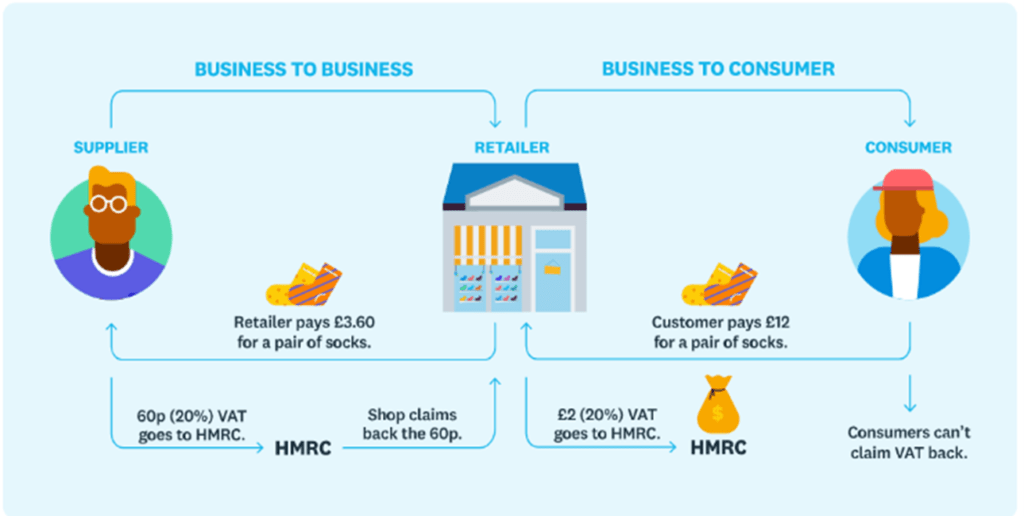

VAT

Value added tax is applicable to businesses with a turnover in excess of £90,000. If your business sells to other businesses (not the public) it is possible to register below this threshold.

VAT is added to every item you sell (at 20%).

When the buyer makes a purchase from a supplier this is called input tax and when a customer makes a purchase from a buyer this is known as output tax.

Businesses registered for VAT must submit (typically quarterly) to the HMRC details of VAT they’ve charged and paid. If they have paid more than charged HMRC will refund the difference otherwise they will need to pay what is owed. This submission has to be submitted digitally from within accounting software (our recommendation is Xero).

The standard VAT rate is 20% but some products and services are subject to lower rates or exempt/zero rated (for example water, most food or children’s cloths).

Please email to request our worksheet to help you decide if you should register for VAT.

HMRC offer a simplified process for businesses with a turnover below £150,000 known as the Flat Rate Scheme. Please ask FD Solutions and Accounting for further details.

Business Rates

You will need to pay business rates if you use any ‘non-domestic properties’ to run your business – this can include a home office.

Business rates are typically paid monthly with annual bill arriving in February or March of each year.

PAYE

If you have employees you are responsible for the PAYE tax (pay as you earn). This is an income tax which is deducted from salaries. These salaries include employees and your own (if your business is a company) and any other director.

You will need to register your business for PAYE with HMRC.

Income Tax rates and bands (frozen until 2028) are

Band

Taxable Income

Tax Rate

Personal allowance

Up to £12,570

0%

Basic rate

£12,571 to £50,270

20%

Higher rate

£50,271 to £150,000

40%

Additional rate

Over £150,000

45%

If you pay employees monthly you must pay their deductions to HMRC by 22nd of the following tax month.

If you pay quarterly you must pay their deductions to HMRC by 22nd of the month following this quarter.

Payroll submissions must be made digitally from within accounting software (our recommendation is Xero).

If you are employing people please be aware of legislation regarding minimum wage, hours and legality to work.

Income Tax

Simply put – this is a tax on income. This is payable on any income earnt as a sole trader, director or partner.

In addition to salary this also covers –

Self-employed profits

State benefits

Pensions

Rental Income (above rent a room scheme)

Trust income

Income on savings (in excess of allowance)

You’ll need to pay your income tax with self assessment by 31st January.

National Insurance

You’ll need to pay National Insurance to qualify for a state pension as well as various government benefits.

Anybody aged over 16 must pay NIC if they are self-employed and making profits in excess of £12,570 or earning more than £241 per week.

National Insurance classes range from 1-4. The type of class you pay varies by employment status, income and whether or not you employ people.

Employed

2024-25 National Insurance

How much you earn

Class 1 Rate

Less than £12,570

0%

£12,570 – £50,270

12%

More than £50,270

2%

Self employed

How much you earn

Class 2 and 4 rates

Less than £6,725

0%

£6,725 – £12,570

£3.45 per week

£12,570 – £50,270

6.00% + £3.45 per week

More than £50,270

2.00% + £3.45 per week

If you are self-employed there are different classes you may fall under

Self-employed: Sole traders must pay Class 2 and Class 4 NIC

Self-employed and employed: Limited company directors who are their own employees must pay Class 1 NICs

As a director you pay NICs through your own PAYE payroll and sole traders must include their contribution in their annual self-assessment.

Which tax type applies to my business?

Sole trader and Partnerships (including LLPs)

Sole traders pay Income Tax on any taxable profits. This is done on an annual basis as part of your self assessment.

For 2024/25 the tax free personal allowance is £12,570 meaning you will not pay income tax until you earn anything beyond that threshold.

Your tax rate also depends on your total annual profit and is distributed as follows –

Basic rate – 20% on profits between £12,571 and £50,270

Higher Rate – 40% between £50,271 and £150,000.

Additional Rate – 45% on profit in excess of £150,001

You must also pay NICs which is a Class 2 flat rate for any profits above £6,725 per annum together with 9% Class 4 if your profits are between £12,570 and £50,270.

Private Limited Company (including CICs)

All companies must pay Corporation Tax on any profits at 19% for the first £50,000 of profits.

There are certain reliefs which can reduce your bill – for example

Claiming research and development relief (R&D) or capital allowances for equipment purchases. For further details please speak to us.

Directors can also pay themselves a dividends (if the company has made a profit). For tax year 2024/25 the first £500 is tax free then – basic rate taxpayers pay 8.75% on dividends, higher rate-taxpayers 33.75% and additional-rate taxpayers 39.35%. There are often tax advantages to taking dividends in lieu of a salary – please ask our accountant for more details.